My Weekly Stock Debrief (July 18 - 22)

Dear subscribers,

Welcome to My Weekly Stock’s debrief for week #29 of 2022 (July 18 - 22), our weekly newsletter reviewing the stock market performance.

1. Market Performance

The equity markets were up for the week, with the SP500 gaining 2.6%, the Dow Jones 2.0%, and the NASDAQ 3.5%. Stronger-than-expected quarterly earnings lifted the stock indexes. The SP500 reclaimed its 50-day moving average, and most of the breadth and technical indicators improved in July.

However, fundamentals will take the center next weeks and decide if this bear market is truly over. In that regard, next week will provide us with critical data and updates.

The busiest week of corporate earnings is upon us with all the tech Mega caps reporting (Microsoft and Alphabet on Tuesday, Meta on Wednesday, Apple and Amazon on Thursday). The FED is meeting next week, and market participants expect a 75bps rate increase. Finally, the GDP numbers for Q2 are released on Thursday and will confirm if the US economy has officially entered in recession.

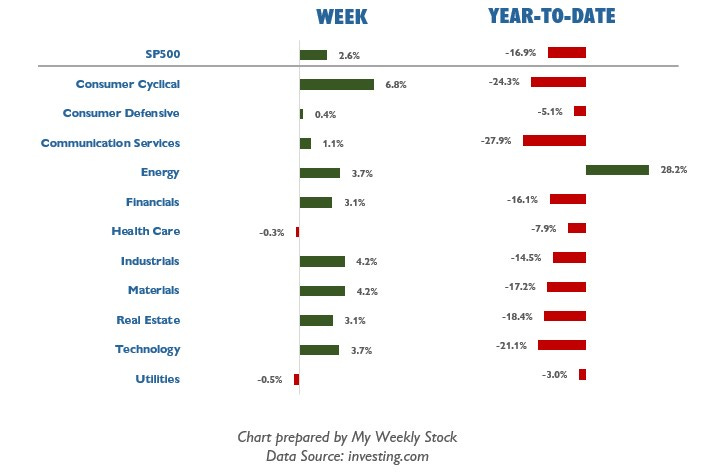

2. SP500 Sector Performance

9 out of the 11 SP500 sectors closed the week higher. Consumer Cyclical and Industrials led this week, finishing up 6.8% and 4.2%, respectively. Utilities and Healthcare lagged and declined by less than 0.5%.

Only 1 sector is positive year-to-date. Energy remains the indisputable winner of 2022 with a 28% gain. Communication Services and Consumer Cyclical are the worst performers in 2022.

3. SP500 Heatmap

80% of the SP500 was up last week. The weekly leaderboard is primarily reflective of the earnings performances. Both Netflix and TSLA were up double-digit after reporting better-than-expected quarterly results.

On the other hand, Verizon (VZ) posted the worst weekly performance of the SP500 due to quarterly results below estimates and a poor outlook for the rest of the year.

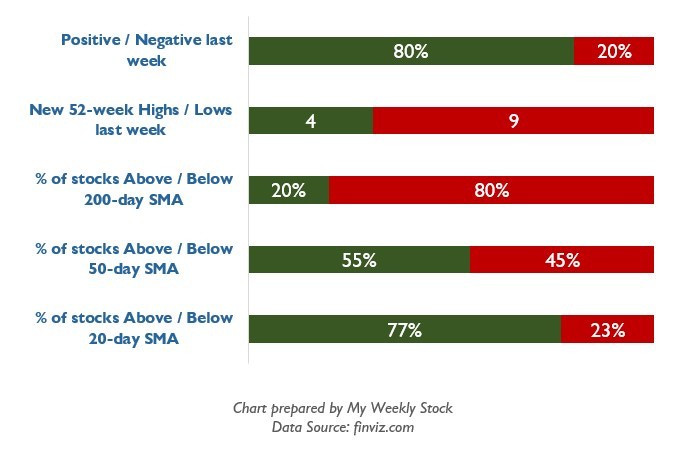

4. SP500 Breadth

Momentum and breadth are improving for the SP500. While 80% of the SP500 stocks are trading below their 200-day moving average, more than half are above the 50-day average. Similarly, almost 80% of the index is above the 20-day.

The number of new 52-week lows has reduced this week, and only 9stocks made a new low.

5. SP500 Daily Chart

The technical indicators are improving as the SP500 reclaimed its 50-day moving average and is still trading above its 20-day one. RSI has a neutral reading of 55 and MACD is positive.

6. Market Sentiment

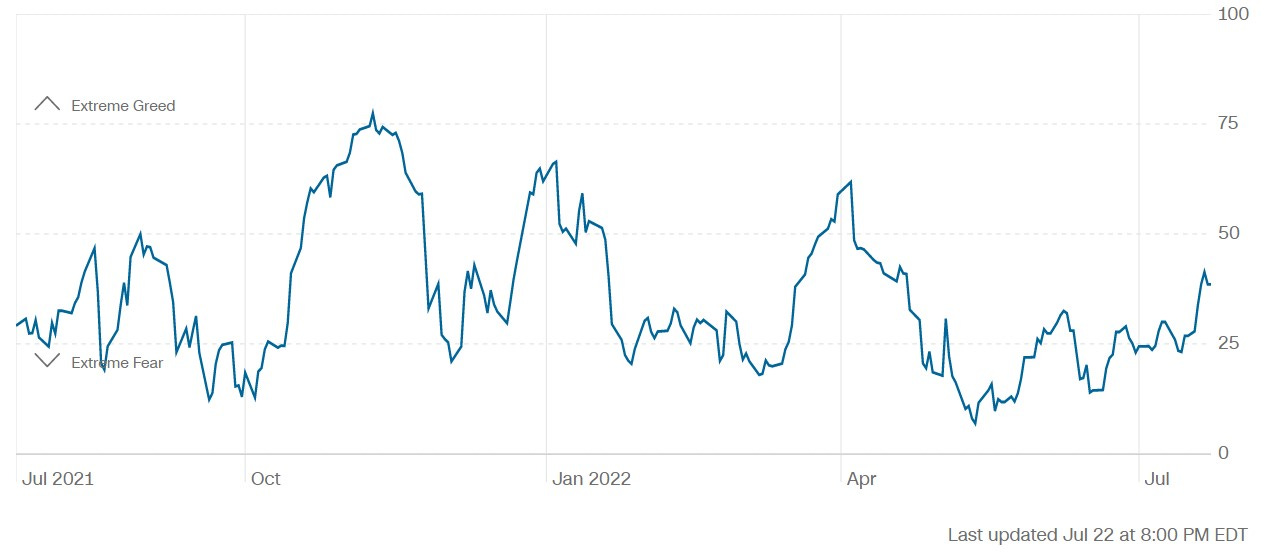

Fear & Greed Index

CNN's Fear & Greed Index tracks seven sentiment indicators and is published daily.

On Friday, the indicator closed at the “Fear” level (39), a 12-point improvement vs. the previous week. The VIX was down 5% and closed at 23, still implying a high level of market uncertainty.

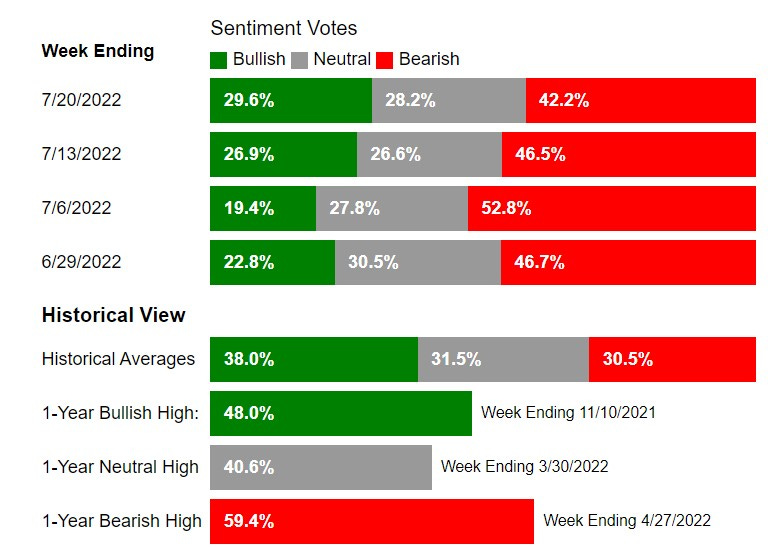

AAII Investor Sentiment Survey

The American Association of Individual Investors surveys each week its members on the direction of the stock market for the next six months. The results are published weekly on Wednesdays.

The last AAII survey reported that 42% of the respondents had a bearish market outlook, which improved from the previous week but remained largely above the historical average.

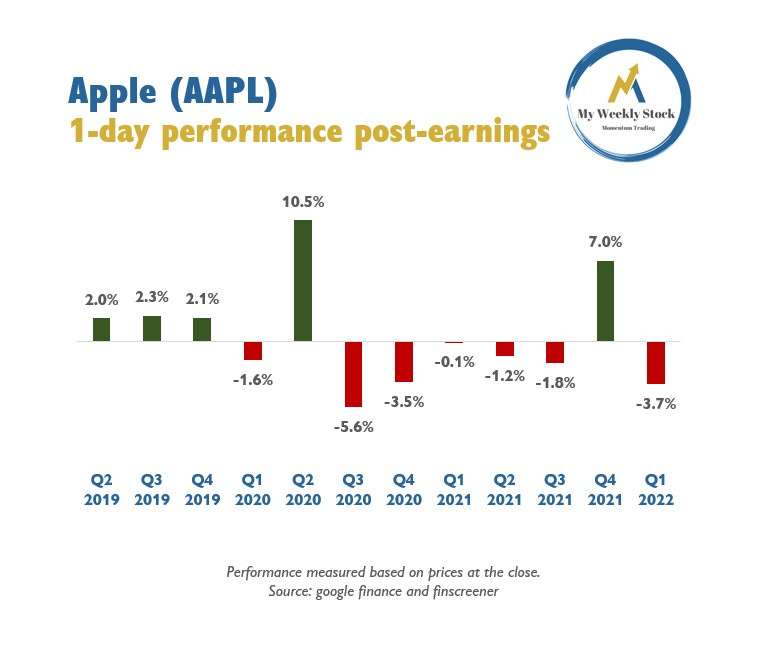

7. Our Earnings Chart of the Week

Apple (AAPL) is reporting earnings next week. The 1-day stock performance post-earnings were positive in 5 of the past 12 quarters, for a daily return of +0.5% and an average move of +/- 3.4% on the earnings day.

8. Our Favorite Analysis of the Week

While stocks staged a most-welcomed rally this week, Mark Minervi reminds us it is not unusual to see periods of significant gains during bear markets but still urges us to navigate this market carefully.

9. The Week Ahead

The busiest week of earnings is upon us, with Alphabet (GOOGL), Microsoft (MSFT), Apple (AAPL), and Amazon (AMZN) reporting quarterly results.

Key economic reports for the week ahead will give us more insights into the economy's strength. GDP numbers for the second quarter are released on Thursday and will confirm if the US economy is officially in a recession. The week's most important event will be the 2-day Federal Reserve meeting, for which the market expects a minimum 75bps interest rate increase.

10. My Weekly Stock Pick

This week, our stock pick was MRK, and the stock was down 5% (Monday open to Friday close). In 2022, My Weekly Stock’s picks are up 6% cumulatively (no leverage, buy and hold for five days), and our options trading is up 147%.

Access our performance tracking here.

We will trade a stock in the Healthcare sector again for the week ahead. Our stock pick will be released on Sunday, and in the meantime, you can learn more about our trading approach in the article below:

Read more about our trading approach here.

And remember to subscribe to My Weekly Stock to receive our stock picks, trading plan, and buy/sell alerts directly in your mailbox.

That’s all for My Weekly Stock’s debrief for week #29 of 2022 (July 18 - 22).

If you enjoy reading our newsletter, please share it via the link below:

You can also follow us on Twitter where we post many more charts during the week.

Have a lovely trading week,

My Weekly Stock

Disclaimer

My Weekly Stock shares information and content on our websites, social networks, or newsletters only for educational purposes. The information contained in our publications has been prepared based on publicly available information and proprietary research. The author does not guarantee the information's correctness, accuracy, or completeness.

All information provided by My Weekly Stock or its affiliates is impersonal and not tailored to your needs, your investment objectives, or your financial situation. Nothing contained in the report shall constitute financial advice or an investment recommendation.

You are solely responsible for your own investment decisions. We recommend consulting with a registered investment advisor, broker-dealer, or financial advisor. If you choose to invest, with or without seeking advice, then any consequences resulting from your investments are your sole responsibility. We are neither liable nor responsible for any profits or losses arising from any investment decision you have taken or made based on information we provide on our websites, social networks, or newsletters.

By using this site, newsletter, or any information provided herein, you indicate your consent and agreement to the terms of this disclaimer.